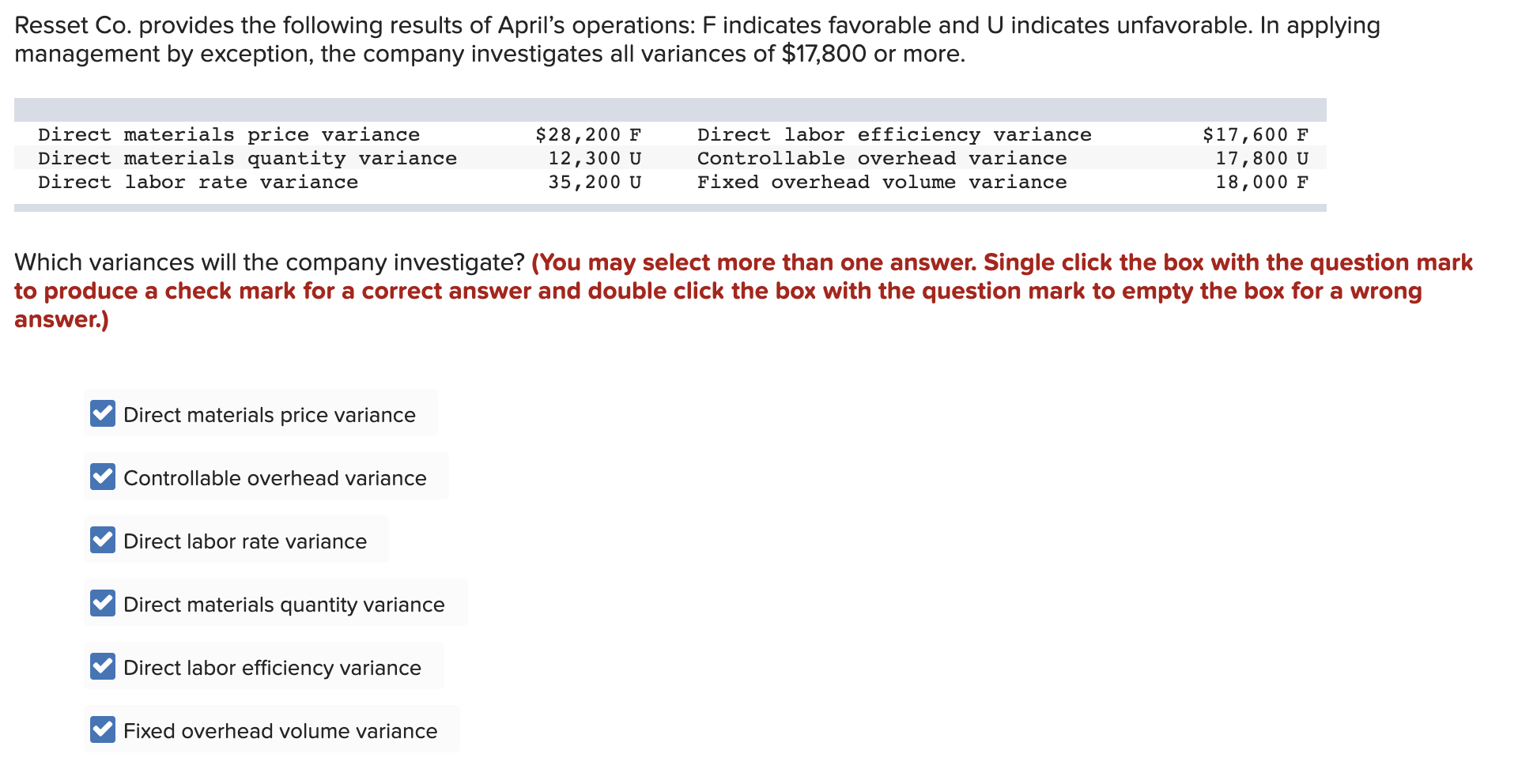

Conversely, it would be unfavorable if the actual direct labor cost is more than the standard direct labor cost allowed for actual hours worked. Let’s assume the standard for direct labor is 3 hours per unit of output and the standard cost for an hour of direct labor is $10. Let’s say the output for the period is 6,000 units and the actual direct labor hours were 18,400 hours and the labor earned $10.30 per hour. The standard direct labor cost for the actual output should have been 18,000 hours (6,000 units of output times 3 standard hours) at $10 per hour for a total of $180,000. Some of that variance is due to the rate being $0.30 too much and some of that variance is due to the direct labor using too many hours—not being efficient.

What is your current financial priority?

An example is when a highly paid worker performs a low-level task, which influences labor efficiency variance. Direct Labor Mix Variance is typically calculated by subtracting the actual amount of labor used from the budgeted amount, then dividing the result by the budgeted amount. Through virtual bookkeeping, one can ensure that business owners are well prepared for their taxes. The bookkeeping service with single entry bookkeeping, double entrybookkeeping, or even accrual bookkeeping makes sure that the transactions are efficiently recorded. These revised transactions help in generating reports, which are ideal for forecasting budgets and double revenue. Only recurring processes benefit from tracking this variance; in cases when commodities are produced infrequently or over a lengthy period of time, tracking this variance serves little purpose.

How can companies reduce Direct Labor Mix Variance?

Once the total overhead is added together, divide it by the number of employees, and add that figure to the employee’s annual labor cost. The material price variance calculation tells managers how much money was spent or saved, but it doesn’t tell them why the variance happened. One common reason for unfavorable price variances is a price change from the vendor. The direct labor (DL) variance is the difference between the total actual direct labor cost and the total standard cost.

Types of Labor Cost Variance

It’s particularly useful in sectors with significant labor costs, such as manufacturing, construction, and services. The standard number of hours is the industrial engineers’ best guess as to the ideal rate public accounting vs private accounting at which the production team can produce things. Thus, it is extremely challenging to establish a standard that you can effectively compare to actual results due to the large number of factors involved.

Comparison of Labor Price Variance vs. Labor Efficiency Variance

For example, advanced tools like SmartBarrel’s workforce management solutions provide real-time insights into labor usage on the construction site. It gives you accurate data on direct labor hours, so you’ll be able to quickly identify inefficiencies and eradicate them before they impact the project’s budget. It occurs when the actual hours worked are more than the standard hours allotted for a specific level of production. In such cases, the negative variance indicates lower efficiency, as more time than expected was needed to complete the work.

Sales Quantity Variance: Definition, Formula, Explanation, And Example

Its core function lies in quantifying this difference, providing insight into whether a business optimally leverages its labor force. A positive variance signals higher efficiency, contrasting a negative variance that suggests lower productivity than projected. It is necessary to analyze direct labor efficiency variance in the context of relevant factors, for example, direct labor rate variance and direct material price variance. It is quite possible that unfavorable direct labor efficiency variance is simply the result of, for example, low quality material being procured or low skilled workers being hired. All tasks do not require equally skilled workers; some tasks are more complicated and require more experienced workers than others.

The total actual cost direct labor cost was $1,550 lower than the standard cost, which is a favorable outcome. The difference in hours is multiplied by the standard price per hour, showing a $1,000 unfavorable direct labor time variance. The net direct labor cost variance is still $1,550 (favorable), but this additional analysis shows how the time and rate differences contributed to the overall variance. Labor price variance, or rate variance, measures the difference between the budgeted hourly rate and the actual rate you pay direct labor workers who directly manufacture your products.

- Labor efficiency variance is calculated by comparing the actual hours worked with standard hours allowed, both at the standard labor rate.

- The direct labor rate variance is the $0.30 unfavorable variance in the hourly rate ($10.30 actual rate Vs. $10.00 standard rate) times the 18,400 actual hours for an unfavorable direct labor rate variance of $5,520.

- By measuring deviations in labor usage, businesses can identify areas of inefficiency, wastefulness, or overperformance.

- Understanding these can help you identify potential issues and implement corrective actions.

The unfavorable variance tells the management to look at the production process and identify where the loopholes are, and how to fix them. Standard costing plays a very important role in controlling labor costs while maximizing the labor department’s efficiency. This variance tells us how efficient the direct labor was in making the actual output that was produced by the direct labor. The most common causes of labor variances are changes in employee skills, supervision, production methods capabilities and tools. SmartBarrel makes 100% accurate time tracking stupid simple — saving you hours every week, keeping your job costs on track, and eliminating all payroll disputes.

This is a favorable outcome because the actual rate of pay was less than the standard rate of pay. In this case, the actual hours worked are 0.05 per box, the standard hours are 0.10 per box, and the standard rate per hour is $8.00. This is a favorable outcome because the actual hours worked were less than the standard hours expected. According to the total direct labor variance, direct labor costs were $1,200 lower than expected, a favorable variance. The difference column shows that 100 extra hours were used vs. what was expected (unfavorable). It also shows that the actual rate per hour was $0.50 lower than standard cost (favorable).